As I moved on to university, everyone around me was hyping up the thrilling aspects of college life—making new friends, joining clubs, and enjoying endless freedom. Caught up in the excitement of it all, I completely overlooked the fundamental requirement for all these adventures: money.

I’m no stranger to budgeting. Since the age of twelve, my parents gave me a weekly allowance as a way to instill financial responsibility.

Yet I’ve come to recognize that managing a budget in university is a whole different ball game compared to my teenage years. Living in my parents’ house, I only had to think about my wants. My expenses mostly went to clothes, books, occasional eating out with friends, and so on.

Now as a university student, I must also consider what I need. Essentials such as food, phone service, and transportation have become crucial items that I must account for. It dawned on me that without careful financial planning, I might not have enough money to cover even the most basic necessities. After many trial and errors, I’ve summarized what I have learned into insights that other students might find valuable.

Lessons learned: Useful tips and resources

1. Write down your necessary expenses and fixed income.

First, list out where you have to spend money, which includes essential needs such as food, laundry, phone bills, etc. Approximate how much each of these items costs and calculate the total. Next, write down your fixed income and the amount. An example might look like this:

The objective here is to estimate your disposable income. This process will help you accurately assess how much money you can allocate to buying things you want (e.g. clothes, going out with friends, eating out).

2. Manage your wants

Once you have a rough estimate of the cost of your essential needs, it’s time to consider your wants. What do you like to spend extra money on, and how much do these indulgences typically cost? Answering these questions can be challenging because your wants often crop up unexpectedly. The most effective approach is to keep a record of your discretionary spending and assess whether it aligns with your budget. If you find that your spending on wants is becoming excessive to the point where it threatens your budget for necessities, it’s a sign that you must make adjustments.

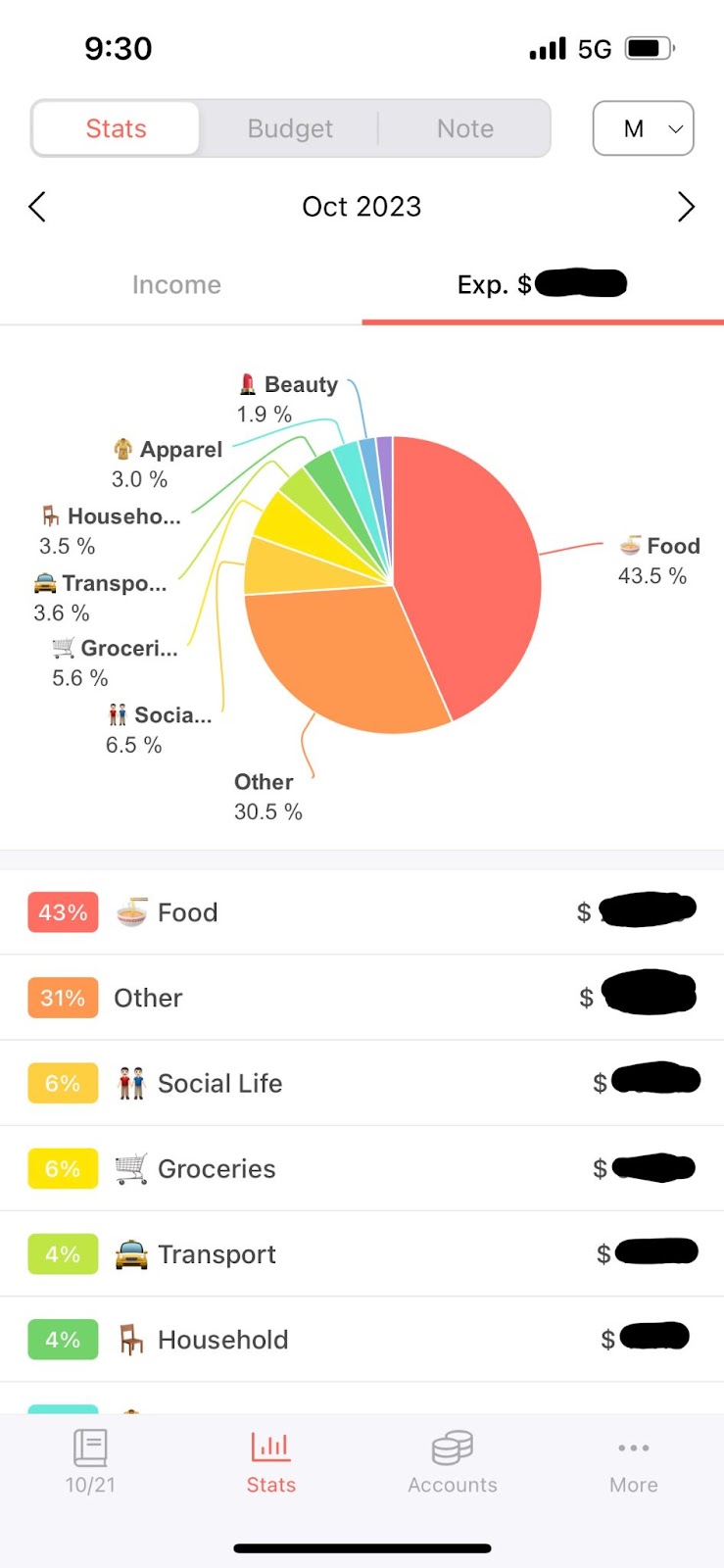

3. Use an expense tracker app

I recommend the application Money Manager because it’s free and easy to use.

Download the app on your phone and make an entry every time an expense occurs. The app has a “Stats” page that automatically tallies your expenditures in specific categories. Reviewing this data weekly helps you to pinpoint high-spending areas and brainstorm ways to cut back on certain expenses.

For instance, I noticed that I was overspending on groceries by buying expensive Greek yogurt and fruit. I’ve since decided to substitute those with cheaper options.

4. Save

Budgeting can be a stressful process. Financial situations can be unpredictable, and unforeseen expenses are bound to occur. Setting aside a fixed monthly amount for savings is an immensely helpful practice that will alleviate this stress. Saving not only brings tangible financial benefits for the future but also offers psychological security, as reflecting on how much you’ve saved will provide a reassuring sense of financial stability.

I strongly recommend opening up an installment savings account. This ensures a consistent monthly deposit, automating your saving routine. It’s a practical step toward securing your financial future and reducing the stress associated with budgeting.

Conclusion (TL;DR: It’s okay to fail)

Much like any other skills, managing finances takes time to perfect. It’s almost inevitable that you will find yourself indulging in frivolous items, overpriced meals, and impulse shopping (I am definitely speaking from personal experience). What is important is that you learn from your mistakes by setting a budget.

Even though there may be times when you struggle to adhere to it, the real objective of budgeting lies in understanding the patterns of your spending and developing an awareness of your financial habits.